Tables

Each table is structured to support efficient querying and data integrity, aligning with Midaz’s commitment to scalability and flexibility.

Table: organization

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Organization. |

| legalName | text | The legal name of the Organization. |

| parentOrganizationId | uuid | The unique identifier of the parent Organization. |

| doingBusinessAs | text | The trade name of the Organization. |

| legalDocument | text | The document of the Organization. |

| status | jsonb | Information about the status. |

| address | jsonb | Information about the address of the Organization. |

| metadata | jsonb | Key-value pairs to add as metadata. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | The timestamp of soft deletion, if applicable (UTC). |

Table: ledger

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Ledger. |

| organizationId | uuid | The unique identifier of the Organization. |

| name | text | The name of the Ledger. |

| status | jsonb | Information about the status. |

| metadata | jsonb | Key-value pairs to add as metadata. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: asset

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Asset. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| name | text | The name of the Asset. |

| type | enum | The type of Asset (currency, crypto, commodity, others). |

| code | text | The code used to refer to the Asset. |

| status | text | Information about the status. |

| metadata | jsonb | Key-value pairs to add as metadata. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: account-type

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Account Type. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| name | text | Name of the Account Type. |

| description | text | Description of the Account Type. |

| keyValue | text | Custom value defined by the user to identify the Account Type. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: account

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Account. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| assetCode | text | The code used to refer to the Asset. |

| name | text | The name of the Account. |

| alias | text | A unique, user-friendly identifier for the account. |

| type | text | The type of account. |

| parentAccountId | uuid | The unique identifier of the Parent Account. |

| entityId | text | The unique identifier of the Entity responsible for the Account. |

| portfolioId | uuid | The unique identifier of the Portfolio. |

| segmentId | uuid | The unique identifier of the Segment. |

| status | jsonb | Information about the status. |

| metadata | jsonb | Key-value pairs to add as metadata. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: portfolio

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Portfolio. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| entityId | text | The unique identifier of the user responsible for the Portfolio. |

| name | text | The name of the Portfolio. |

| status | jsonb | Information about the status. |

| metadata | jsonb | Key-value pairs to add as metadata. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: segment

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Segment. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| name | text | The name of the Segment. |

| status | jsonb | Information about the status. |

| metadata | jsonb | Key-value pairs to add as metadata. |

| created_at | timestamptz | Timestamp of creation (UTC). |

| updated_at | timestamptz | Timestamp of last update (UTC). |

| deleted_at | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: balance

| Column | Type | Description |

|---|---|---|

| id | text | The unique identifier of the Balance. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| accountId | uuid | The unique identifier of the Account. |

| alias | text | The alias for the account used in the operation. |

| assetCode | text | The code used to refer to the Asset. |

| available | text | Previous available balance. |

| onHold | text | Amount on hold/reserved. |

| version | integer | Balance version, which is updated with each transaction. |

| accountType | text | The type of account. |

| allowSending | boolean | If true, indicates that sending transactions is permitted. |

| allowReceiving | boolean | If true, indicates that receiving transactions is permitted. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: operation-route

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Operation Route. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| title | text | Short text summarizing the purpose of the operation. Used as an entry note for identification. |

| description | text | Detailed description of the Operation Route purpose and usage. |

| type | text | The type of operation (debit/credit). |

| account | jsonb | Defines the rule for selecting the account that will participate in the operation (debit or credit). |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: operation

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Transaction Route. |

| transactionId | uuid | The unique identifier of the Transaction. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| accountId | uuid | The unique identifier of the account of which you want to retrieve the balances. |

| balanceId | uuid | The unique identifier of the Balance. |

| accountAlias | text | The alias for the account used in the operation. |

| description | text | Description of the transaction. |

| type | text | The type of the operation (debit or credit). |

| assetCode | text | The name of the asset used in the operation. |

| chartOfAccounts | text | [Deprecated] The name of the Chart-of-Accounts that the operation belongs to. |

| route | text | The chart of accounts group name that categorizes the operation under a specific group. |

| amount | jsonb | An object containing information about the amount used in the operation. |

| balance | jsonb | An object containing information about the balance before the operation. |

| balanceAfter | jsonb | An object containing information about the balance after the operation. |

| status | jsonb | The transaction status (pending, completed, reversed). |

| metadata | jsonb | Key-value pairs to add as metadata. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: transaction-route

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the Transaction Route. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| title | text | Short text summarizing the purpose of the transaction. Used as an entry note for identification. |

| description | text | A description for the Transaction Route. |

| operationRoutes | array | A list of Operation Route IDs that define the debit and credit logic for the transaction. |

| metadata | object | Key-value pairs to add as metadata. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

Table: transaction

| Column | Type | Description |

|---|---|---|

| id | uuid | The unique identifier of the transaction. |

| organizationId | uuid | The unique identifier of the Organization. |

| ledgerId | uuid | The unique identifier of the Ledger. |

| description | text | Description of the transaction. |

| route | text | The chart of accounts group name that categorizes the operation under a specific group. |

| status | jsonb | Information about the status. |

| amount | text | The sent amount. |

| assetCode | text | The code used to refer to the Asset. |

| chartOfAccountsGroupName | text | [Deprecated] The name of the group used to categorize the operations of a transaction under the same group. |

| source | array | The list of accounts used as source. |

| destination | array | The list of accounts used as destination. |

| operations | array | The list of operations in the transaction. |

| metadata | jsonb | Key-value pairs to add as metadata. |

| createdAt | timestamptz | Timestamp of creation (UTC). |

| updatedAt | timestamptz | Timestamp of last update (UTC). |

| deletedAt | timestamptz | Timestamp of soft deletion, if applicable (UTC). |

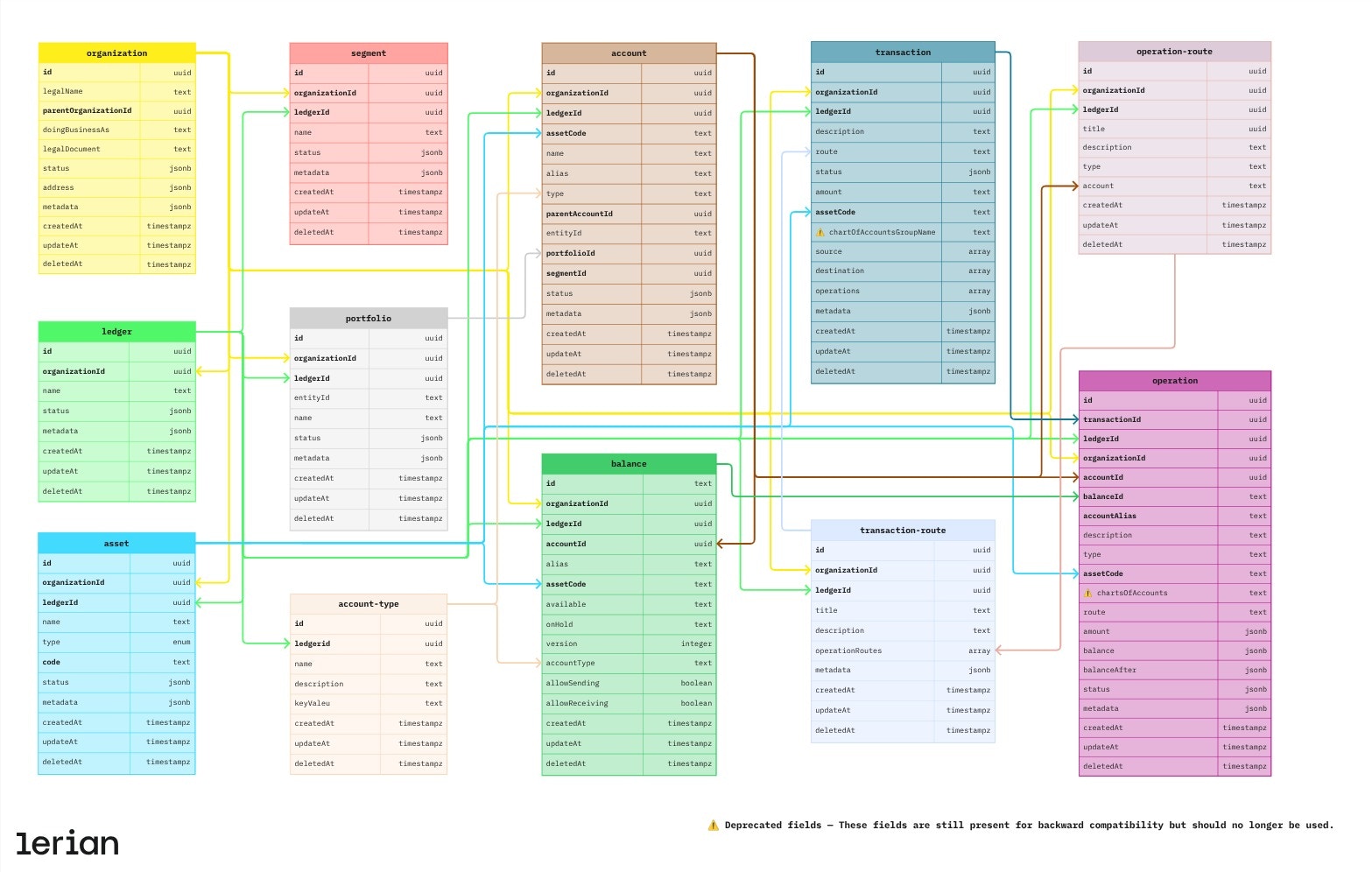

Data model

In Figure 1, you can find a visual representation of the core tables in Midaz and their relationships. The diagram helps developers and DB administrators understand how the different entities are interconnected within the system, serving as a guide for efficient data handling and integration.

Figure 1. Midaz tables and their relations.